Gold is one of the rare assets that sits at the intersection of emotion, tradition, and investing. Its role as an investment vehicle has been endlessly debated. For gold bugs, it is the ultimate hedge against the debasement of fiat currency, a chaos-insurance policy that has survived for millennia. For sceptics (Warren Buffett being the most famous), it is a pet rock: an asset that produces no cash flow, pays no dividends, incurs storage costs, and relies entirely on the greater fool theory for price appreciation.

So does holding gold actually improve long-term investment outcomes?

We’ve analysed the data, and the answer, like most things in finance, is nuanced. It depends entirely on whether you view gold as an investment or as insurance.

The Pet Rock Problem

The primary argument against gold is mechanical: it has no internal rate of return. When you own a stock, you own a claim on future earnings. When you own a bond, you own a claim on interest payments. When you own gold, you own a metal that sits in a vault and does absolutely nothing until you sell it.

Long-term data reflects this reality. Rolling return analysis removes the comfort of cherry-picked start dates and shows what happens when an investor enters the market at any point in time and holds for a fixed horizon. Since the mid-2000s, rolling return data clearly shows that equities dominate gold across most meaningful investment horizons.

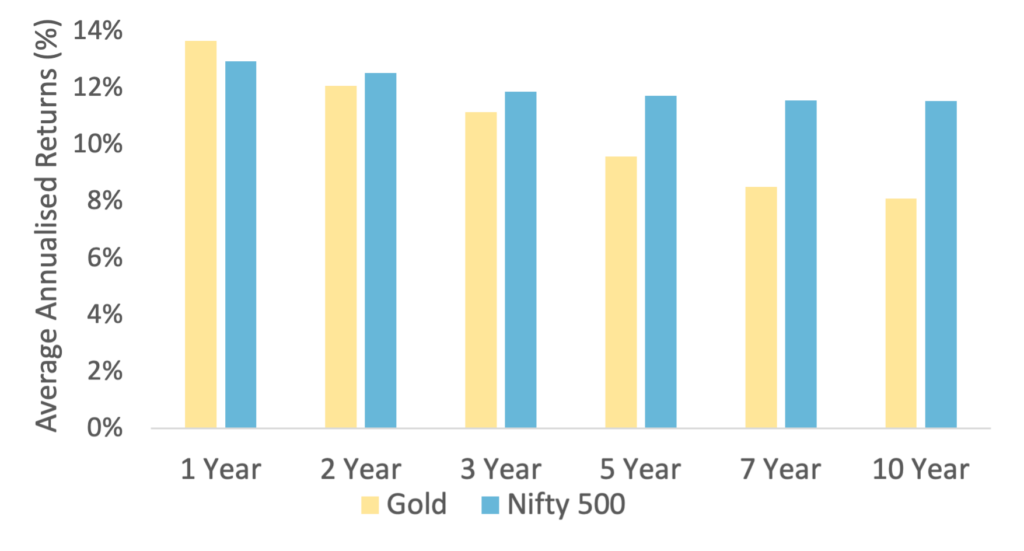

Since 2007, across two-, three-, five-, seven-, and ten-year rolling periods, the Nifty 500 has outperformed gold on average. As shown in Figure 1, gold’s relative performance deteriorates steadily as the investment horizon lengthens.

Figure 1: Average Annualised Rolling Returns (Gold vs. Nifty 500)

As the holding period increases, gold’s odds of beating equities decline sharply as well. At the one-year mark, gold outperforms roughly half the time. Stretch the horizon to five years, and that probability drops below 30%. Over seven- and ten-year periods, gold not only underperforms on average, but does so with increasing consistency.

| Time Period | 1Y | 2Y | 3Y | 5Y | 7Y | 10Y |

| Average Outperformance of Gold | 0.72% | -0.45% | -0.72% | -2.14% | -3.07% | -3.44% |

| Probability of Outperforming Nifty 500 | 50.00% | 46.00% | 45.74% | 29.88% | 20.71% | 26.92% |

The takeaway is not that gold never wins, but that without earnings, cash flows, or reinvestment, gold struggles to keep up with assets that compound through economic growth.

The Case for Gold: Correlation, Not Returns

Gold’s primary value lies not in its long-term return potential, but in its correlation profile. Historically, gold has exhibited low, and at times negative, correlation with both equities and bonds. This is the often-cited free lunch of diversification: gold tends to zig when the rest of the portfolio zags.

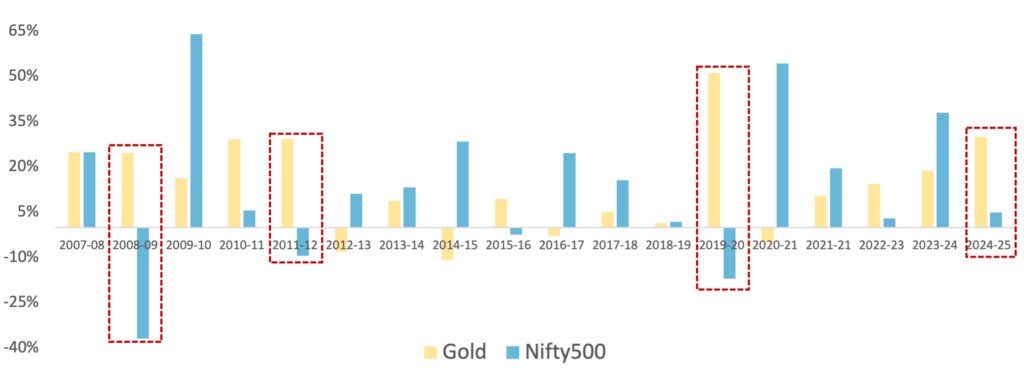

During periods of severe equity drawdowns, such as the 2008 global financial crisis, the 2011 market fall, the onset of COVID in early 2020, and the recent geopolitical instability, gold has delivered positive returns even as equities fell sharply.

Academic research describes this behavior as flight to safety. When growth expectations collapse and risk aversion spikes, capital moves away from risky assets and toward perceived stores of value. Gold has historically been one of the primary beneficiaries of this shift.

Figure 2: Gold as a Flight-to-Safety Asset During Market Crises

That said, this protection comes at a cost. Outside of crisis periods, gold frequently underperforms. There are long stretches where gold delivered little to no returns while equities continued to compound steadily.

The Cyclical Trap: Silence vs. Violence

Gold is a deeply cyclical asset. It does not compound gradually. Its history is characterised by long stretches of silence punctuated by short, violent rallies.

- The Rallies: 2008–2012, 2019–2020, and the recent surge in 2024–2025.

- The Silence: 2013–2019, gold effectively went nowhere, while equities compounded steadily.

This pattern is not accidental. Gold does not grow through productivity, innovation, or earnings expansion. It reprices episodically, typically during periods of financial stress, inflation shocks, or elevated uncertainty. As a result, much of gold’s long-term return is concentrated in a handful of short, stress-driven windows.

Investors who attempt to use gold as a growth asset are therefore forced into a timing game: identifying when fear, inflation, or monetary disorder will spike. Most investors fail at this. Passive holders endure years of opportunity cost while waiting for the next crisis, even as productive assets continue to advance.

The Safety and Liquidity Myths

Gold’s popularity is often also justified on the grounds of safety and liquidity, but both claims are increasingly overstated. Much of household gold exposure still comes through physical holdings and jeweller-run schemes, which involve making charges, purity risk, storage costs, and limited investor protection. Calling these arrangements safe while dismissing regulated, transparent market instruments as complex is a triumph of narrative over logic.

The liquidity argument has aged just as poorly. The idea that gold is uniquely liquid because it can be pawned in emergencies belongs to another era. Today, investors can borrow against mutual funds and equities, often at competitive rates, without selling the underlying asset. Liquidity is no longer gold’s exclusive advantage.

So how should gold actually be used in a portfolio?

If you are looking for an asset to make you rich, gold is the wrong tool. Productive assets like equities are the engines of long-term wealth creation. Gold makes sense only as insurance: something that smooths portfolio volatility, even if that means tolerating long stretches of underperformance. Used sparingly and with realistic expectations, gold earns its place not as a growth engine, but as a shock absorber.

Gold is not an investment in human ingenuity. It is a hedge against chaos. The more relevant question, therefore, is not whether to hold gold, but how much insurance your portfolio needs.

Hi, this is a comment.

To get started with moderating, editing, and deleting comments, please visit the Comments screen in the dashboard.

Commenter avatars come from Gravatar.