“Don’t look for the needle in the haystack. Just buy the haystack!” ― John C. Bogle

Index funds are often presented as the rational choice, the grown-up solution for anyone serious about long-term wealth creation. Low cost, diversified, emotion-free. No manager risk. No second-guessing.

And to be fair, this narrative did not emerge without reason.

Over long periods, broad market indices have delivered respectable returns. They have outperformed a large number of actively managed funds, especially after costs. So for investors who want simplicity, discipline, and protection from bad decisions, index investing makes sense. It offers something rare in finance: a strategy that is both effective and easy to stick with.

But does that mean the Index is unbeatable?

The data does not support that conclusion. While it is true that many active funds fail to beat the index, it does not follow that active management itself is futile. The real mistake is treating all active strategies as the same. They aren’t. When done right, active management can meaningfully change outcomes and outperform the index significantly.

So what happens when we actually test this?

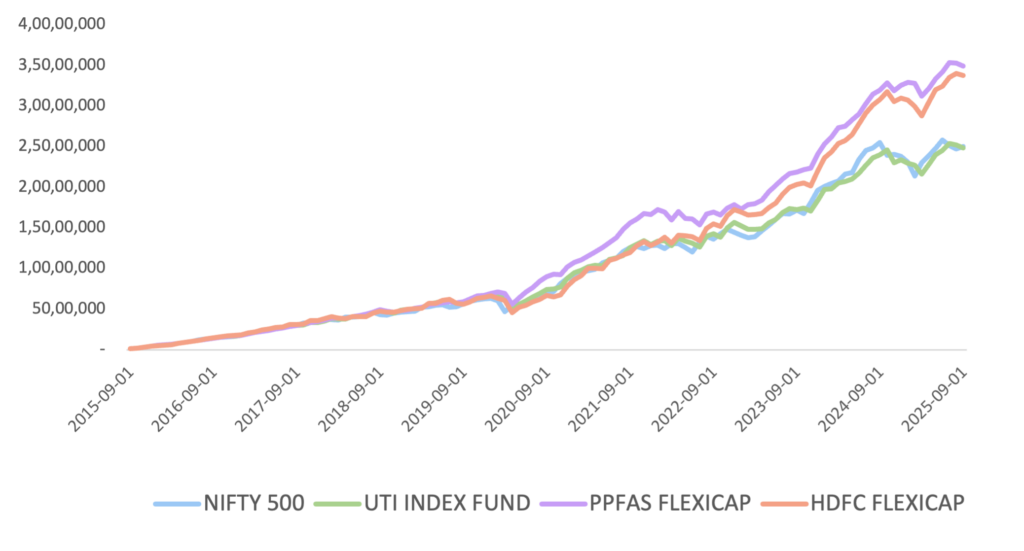

Rather than debating philosophy, we tested the claim. We ran a simple, real-world experiment. A monthly SIP of ₹1,00,000 invested consistently for 10 years, from September 2015 to September 2025 across:

- Nifty 500 – broad market proxy

- UTI Nifty 50 Index Fund

- Parag Parikh Flexi Cap Fund

- HDFC Flexi Cap Fund

Two index representations. Two actively managed, large, well-established flexicap funds. Over this decade, the total amount invested came to ₹1.2 crore. These were the returns:

| Nifty 500 | UTI Index Fund | PPFAS | HDFC Flexi | |

| XIRR | 14.06% | 13.93% | 20.24% | 19.62% |

| Final Value | 2,50,32,481 | 2,48,54,346 | 3,49,13,411 | 3,37,63,469 |

Figure 1: SIP Portfolio Value Over Time — Index vs. Active Funds (2015–2025)

The index delivered exactly what it promises: steady, respectable returns. But the actively managed funds did something more. They delivered an XIRR that is approximately 5-6% higher than the index, translating into nearly ₹1 crore of additional wealth over a decade.

What’s more important is how this outperformance showed up. It did not come from one lucky year. It did not hinge on a single bull run. As the chart shows, the separation builds slowly and steadily over time. Small annual edges, compounded over a decade.

The takeaway here is not that active funds always win. Many don’t. It is that good active management, applied consistently, can materially improve outcomes. And dismissing it outright because “most funds underperform” throws away that possibility entirely.

But what if investors don’t pick the right funds?

One obvious counter-argument to the comparison above is this: “You picked good active funds. Most investors won’t.”

So we took the argument one level deeper. Instead of relying on individual fund selection, we tested a simple, rule-based strategy.

Every month for the last 10 years we constructed a portfolio using a mechanical process:

Select the top 15 ranked equity funds based on past performance across multiple rolling time frames and rebalance annually using the same criteria. Deduct capital gains tax on rebalancing.

The question was simple: Can a rules-based active strategy outperform the index post taxes?

The answer, was yes. These were the results of our back test.

| Time Frame | 1Y Return | 3Y CAGR | 5Y CAGR | 7Y CAGR | 10Y CAGR |

| Probability of Outperformance | 80.47% | 88.46% | 100.00% | 100.00% | 100.00% |

| Average Outperformance | 6.46% | 3.55% | 2.60% | 2.47% | 3.19% |

Across holding periods, the strategy delivered average excess returns of roughly 2.5% – 6.5% per annum over the index, even after accounting for taxes on churn.

This shows that active management does not need to be perfect to work. It doesn’t require identifying a single “best” fund for the next decade. Even a broad, diversified, rule-driven selection process, applied consistently, can exploit inefficiencies that an index, by design, cannot.

The real myth

Index investing works. It is an excellent default. It protects investors from their worst instincts, keeps costs low, and delivers market returns with remarkable reliability. For many investors, that alone is enough, and that’s perfectly fine.

But that’s the very reason the idea that the index is “unbeatable” survives, because it is good enough for most investors, not because it is the best outcome possible. An index owns everything, makes no decisions and takes no risks beyond the market itself. That simplicity is its strength but also its limitation.

Active management, when done poorly, deserves the criticism it gets. But when done well, it can exploit inefficiencies that an index cannot. Small edges, applied consistently, compound into large differences over time.

Index investing is a great default. But default does not mean optimal.

The real myth isn’t that the index works. It’s that it’s the best you can do.